| 24-Apr-2024

April 21st has been a historic day. The Ecuadorian people voted massively NO in the referendum question about whether Ecuador should return to arbitration.

| 24-Apr-2024

Le 21 avril a été une journée historique. Le peuple équatorien a massivement voté NON à la question référendaire sur un éventuel retour de l’Équateur à l’arbitrage.

Bilaterals.org | 21-Apr-2024

On 21 April 2024, the government of Daniel Noboa is holding a referendum in Ecuador to amend the country’s constitution and, in particular, to reactivate the dangerous investor-state dispute settlement mechanism.

América Latina Mejor sin TLC | 19-Apr-2024

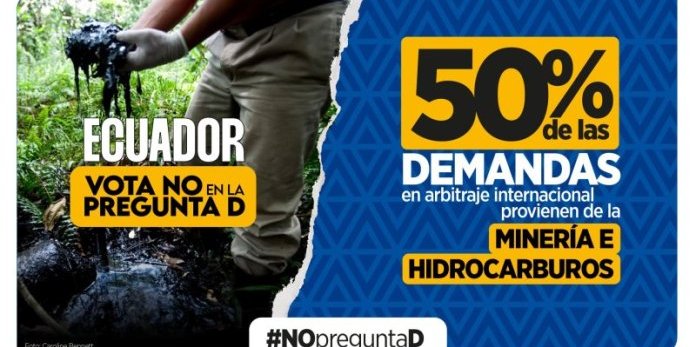

El 21 de abril las ecuatorianas y los ecuatorianos asistirán a las urnas para decidir sobre temas como: el regreso del país al sistema de arbitraje internacional, una reforma laboral regresiva y la participación de las fuerzas armadas en la seguridad interior, entre otros.

Bilaterals.org | 19-Apr-2024

Le 21 avril 2024, le gouvernement de Daniel Noboa organisera un référendum en Équateur, qui vise à modifier la Constitution nationale, et en particulier, à réactiver le dangereux mécanisme de règlement des différends entre investisseurs et États.

Bilaterals.org | 15-Apr-2024

El próximo 21 de abril, el gobierno de Daniel Noboa celebrará un referéndum en Ecuador, que busca realizar cambios en la Constitución Nacional y aborda temas fundamentales como seguridad e inversiones. Dentro de las 11 preguntas que forman parte del referéndum una pregunta en particular, la D, busca reactivar el peligroso mecanismo de solución de controversias inversor-Estado (ISDS).

Global Justice Now | 12-Apr-2024

The Secret World of Investor Courts is a podcast made by the Global Justice Now Youth Network, exploring corporate power, colonialism and climate justice.