SOMO | 5 March 2024

Klesch Group’s legal paradox

by Vincent Kiezebrink and Bart-Jaap Verbeek

Summary

- In October 2023, oil refiner Klesch Group sued the EU over its windfall profits tax through investor-state dispute settlement (ISDS).

- Klesch accuses the EU of using the invasion of Ukraine as a pretext for its “discriminatory” tax, constraining fossil fuel industry competitiveness, and effectively disrupting energy markets.

- In its annual report, however, Klesch describes the invasion of Ukraine as the main reason its Danish refinery boasted a twelvefold increase in profit margin

On 6 October 2022, after the Russian invasion of Ukraine had sent oil and gas prices skyrocketing, the European Council instated its so-called solidarity contribution. This windfall profits tax targeted energy companies which were benefiting from the crisis, and was reportedly aimed at financing mitigation efforts to alleviate the cost of high energy prices for consumers. Throughout 2022, energy prices were the single-largest contributor to EU inflation, and energy inflation reached a record of 44.3% in March of 2022.

Research commissioned by the European Parliament estimated that the total EU revenue gained through the windfall profits tax was likely to amount to €4.4 billion. However, this estimation was based on 2021 profit figures for the energy industry, and the extreme oil and gas price rises of 2022 significantly increased windfall profits tax revenues for EU governments. Revenues from the tax differed heavily between EU member states. The Netherlands and Spain, for example, are expecting to receive €3.2 billion and €2.9 billion in revenues, respectively. Germany, on the other hand, reported revenues of only €417 million, seemingly in part because it applied the windfall tax only for a period that started at the end of 2022 when the peak in oil prices had already passed.

Big Oil’s big windfall

Meanwhile, 2022 was an exceptionally profitable year for companies involved in the energy supply chain. From oil and gas producers to oil refiners, to the energy companies that supply power directly to consumers, increased profits were a common feature of the market. For example, in 2022 the six largest North American and European oil firms doubled their already significant profits, coming to a staggering $219 billion. Of these profits, over half were paid out directly to investors through dividend payments and share repurchases.

And yet, the windfall profits tax appears to have led to much energy industry discontent. There have been many corporate complaints lamenting the decrease in profits caused by the tax. For example, oil and gas producer Harbour Energy complained about the tax while at the same time announcing $1 billion in payouts to investors. Or the association of Spanish power companies decrying the tax as discriminatory and unjustified. Spanish energy company Repsol even threatened to move its investments to other EU countries and predicted a drop in vital energy investments in Spain.

Some companies took their complaints a step further and challenged the European Council’s regulation at the European Court of Justice. These include non-EU energy companies operating in EU tax havens Ireland and the Netherlands, such as Canadian Vermilion Energy, Omani Petrogas Exploration and Development, and US-based ExxonMobil. In December 2023, ExxonMobil and its business partner Shell also sued the Dutch State at an arbitration court, citing the windfall profits tax as one of their reasons.

Income statements show that in 2022, Vermilion Energy’s pre-tax profits rose by 60% from its already exceptional 2021 profits and came to a total of $1.5 billion. Exxon Mobil’s pre-tax profits rose by a staggering 179% in 2022, to a total of $74 billion. Meanwhile, the effective tax rate Exxon Mobil was subject to around the world stayed approximately the same, at around 25%.

Klesch Group sues the EU

Last October, energy company Klesch Group decided to follow suit and initiate its own international arbitration proceedings. The group is owned by billionaire A. Gary Klesch, who was born in the US but now resides in Malta, and who controls the Klesch Group through a string of subsidiaries in tax havens Malta and Jersey. Klesch Group’s main assets are its two oil refineries: Heide refinery in Germany and Kalundborg refinery in Denmark. Its cases against the windfall profits tax relate to these assets: one was filed against the EU, and two against Germany and Denmark where it claims that its refineries are subject to those countries’ windfall profits taxes. Through these cases, Klesch is seeking compensation of at least €95 million.

Klesch Group relies thereby on the Energy Charter Treaty, a multilateral treaty from 1994 that promotes and protects foreign investment in the energy sector. Over the past years, the treaty has attracted much criticism for enabling foreign investors to sue governments and claim compensation for measures in the energy sector that are allegedly in violation of the ECT, including measures that are legitimate and in the public interest. Energy companies have used the ECT to challenge legislation aimed at banning or phasing out oil, gas and coal infrastructure and other environmental measures as well as changes in subsidy schemes and feed-in tariffs for renewable energy. By prioritizing regulatory stability and predictability for investors, the ECT significantly constrains the policy space of governments to act, particularly in times of energy transition and crisis.

This has led to the UN’s Intergovernmental Panel on Climate Change (IPCC) warning that the ECT, among other international investment agreements, “may lead to ‘regulatory chill’, which may lead to countries refraining from or delaying the adoption of mitigation policies, such as phasing out fossil fuels”. Its use now by Klesch Group may have a similarly chilling effect on future windfall profits taxation in the European Union.

Despite attempts to modernize the ECT, ten EU member states, including Germany and Denmark, have already announced their intentions to withdraw from the treaty, with the European Commission proposing a coordinated EU exit altogether.

EU member states are currently set to vote on such a proposal in the Council after months of political deadlock. If adopted, this would allow the EU and all EU member states to leave the treaty while offering the possibility for those states that want to sign up to the reformed treaty, even though those reforms are modest and their effectiveness remains highly uncertain.

Klesch’s duplicity

A leaked internal EU briefingdescribes how Klesch Group accuses the EU of using the Russian invasion of Ukraine as a pretext to implement its “arbitrary, discriminatory, retroactive and punitive” windfall profits tax, thereby constraining fossil fuel companies’ competitiveness. Klesch appears to imply that the EU has acted in bad faith – high energy prices were not the reason for a windfall profits tax, they were a pretext.

However, what Klesch alleges in its arbitration filings seems to contradict its own annual reporting. Klesch’s Danish subsidiary Kalundborg Refinery AS states the following in its 2022

annual accounts:

“Our financial results for 2022 have been very strong as a result of the high refining margins, which was driven by the Russian invasion of Ukraine, the resulting sanctions and impact on product flows. […] The 2022 financial results were highly impacted by the steep spike in the refining margin, as a result of the market disruption caused by the Russian invasion of Ukraine.”

From: 2022 annual accounts of Klesch’s Danish subsidiary Kalundborg Refinery AS

Where in arbitration Klesch Group claims that EU intervention would limit their competitiveness as it disrupts the European energy market, in its annual accounting the company states instead that markets were disrupted by the invasion of Ukraine, which has greatly benefitted its profitability, thereby increasing the company’s overall competitiveness. In the arbitration, Klesch Group calls the invasion of Ukraine a pretext used by the EU to levy additional taxes which would disrupt energy markets, while in its own corporate reporting, the company says it is the cause of a disruption in European energy markets.

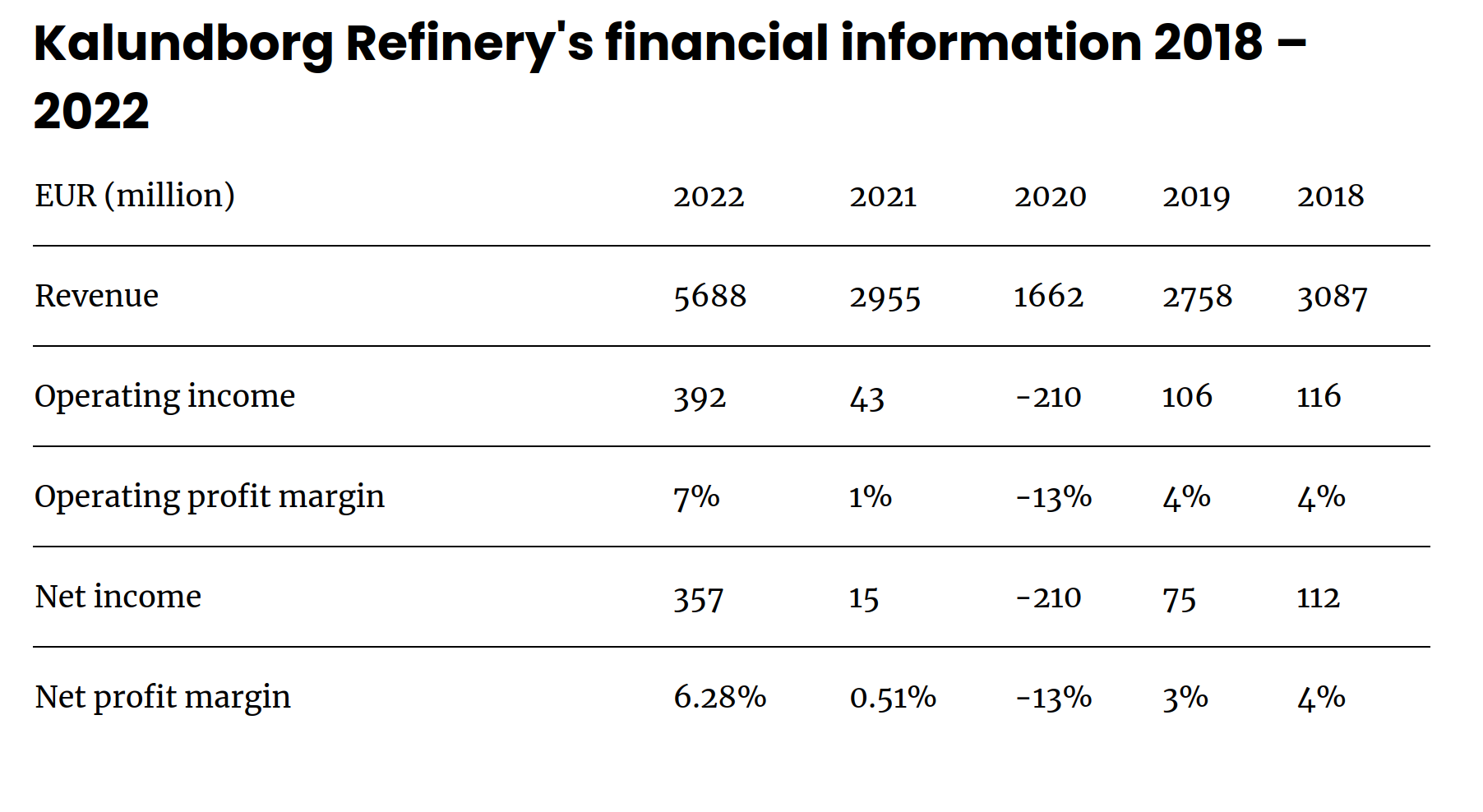

And this energy market disruption is reflected in Kalundborg Refinery’s financial figures for 2022. Between 2021 and 2022, the company’s revenues increased by 92%, its net profits increased by 2280% from EUR15 million to EUR357 million, and its net profit margin increased from 0.5% to 6.3%. The company’s 2022 profits are more than twice as high as in any previous year.

There appear to be two – potentially coinciding – explanations for these record profits. It could be that the dramatic increase in prices Kalundborg Refinery charged its buyers vastly outweighed the increased price its suppliers were charging for unrefined oil, allowing the operation to become much more profitable. Alternatively, Kalundborg Refinery may have stored oil it purchased when prices were low, and sold that oil as prices rose, allowing the company to increase its profit margin. From its profits, Kalundborg Refinery paid out a EUR118 million extraordinary dividend in 2022.

Although the exact argumentation underlying Klesch’s arbitration case is not publicly available, the company appears to claim that the windfall profits tax limits its competitiveness when compared to competitors in non-EU countries without windfall profits taxes, or to competitors in the EU whose lower profits means they are not subject to the tax. Notably, the EU windfall profits tax only taxes the segment of corporate profits which are 20% higher than the previous years’ average. Whatever amount exceeds that average by 20% is then taxed, at 33% in the cases of Denmark and Germany. The prospect that a company which has enjoyed record profits would see its competitiveness endangered by an additional tax targeted specifically at its windfall profit, seems extremely unlikely at best.

Windfall profits tax: the solution, not the problem

Widely acclaimed research by Isabella Weber and Evan Wasner details how oil producers responded to supply-chain shortages by increasing prices, not just to cover their costs and maintain profit levels, but to substantially increase their profit margins. Because oil companies had decreased their production as a result of the COVID-19 pandemic, supply was limited due to the Russian invasion of Ukraine, and the end of the pandemic caused a surge in the demand for oil, oil-producing companies with large market shares found themselves enjoying temporary monopolies of sorts, giving them the power to set higher prices. Companies further down in the oil supply chain (e.g. traders and refiners) similarly enjoyed an increase in market power due to the shortages, and magnified these price hikes, increasing their own profit margins as well.

To curb what Weber and Wasner call seller’s inflation, countries should consider implementing price gouging laws that limit sellers’ ability to rapidly raise prices in times of crisis, and – importantly –governments should levy windfall taxes to disincentivize companies from raising prices to increase their profit margins. In that sense, the EU’s windfall profits tax for energy producers was a small step in the right direction. Instead of giving in to corporate protests, whether verbal or legal, the EU should revisit this momentum, to explore how a more permanent windfall profits tax could be implemented. The EU needs to make use of this historic opportunity to exit the Energy Charter Treaty and safeguard its member states’ capacity to stop this kind of corporate profiteering.