CAN Europe | 25-Apr-2024

The European Parliament voted today largely in favour of the Commission’s proposal for the European Union to withdraw from the Energy Charter Treaty, a landmark move that campaigners across Europe have been demanding for years.

TNI | 24-Apr-2024

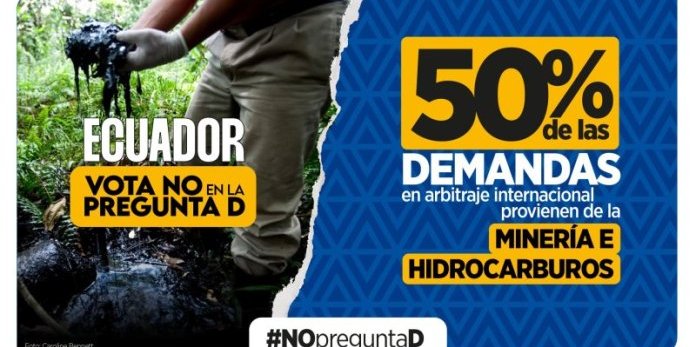

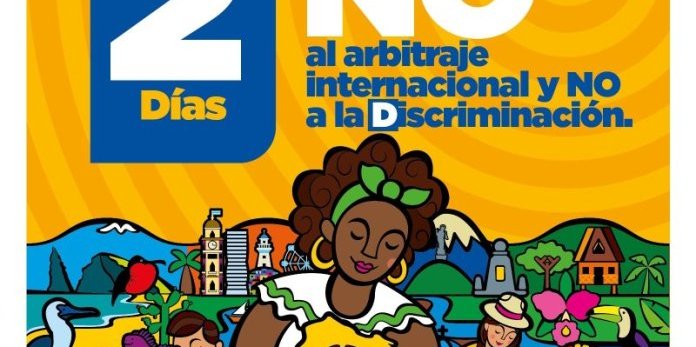

El domingo 21 de abril ha sido un día histórico. El pueblo ecuatoriano votó masivamente por el NO en la pregunta del referéndum sobre si el Ecuador debía volver al arbitraje.

CNCD 11.11.11 | 24-Apr-2024

Ce 24 avril, les parlementaires européens ont approuvé en séance plénière la proposition de décision du Conseil visant à permettre à l’Union européenne de se retirer du Traité sur la Charte de l’énergie.

| 24-Apr-2024

April 21st has been a historic day. The Ecuadorian people voted massively NO in the referendum question about whether Ecuador should return to arbitration.

| 24-Apr-2024

Le 21 avril a été une journée historique. Le peuple équatorien a massivement voté NON à la question référendaire sur un éventuel retour de l’Équateur à l’arbitrage.

Bilaterals.org | 21-Apr-2024

On 21 April 2024, the government of Daniel Noboa is holding a referendum in Ecuador to amend the country’s constitution and, in particular, to reactivate the dangerous investor-state dispute settlement mechanism.

América Latina Mejor sin TLC | 19-Apr-2024

El 21 de abril las ecuatorianas y los ecuatorianos asistirán a las urnas para decidir sobre temas como: el regreso del país al sistema de arbitraje internacional, una reforma laboral regresiva y la participación de las fuerzas armadas en la seguridad interior, entre otros.